Start-up Business Loan

HBDI can make loans to businesses that are just getting started and have yet to generate any cashflow. Typically, a start-up loan will range from $25,000 up to $75,000. The requirements to obtain a start-up loan include the following:

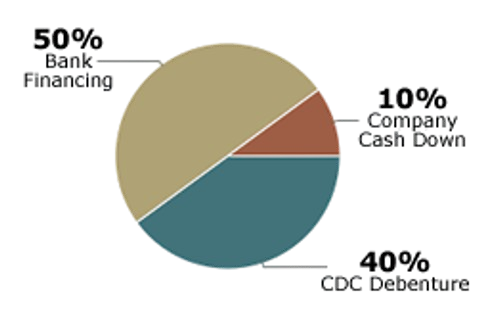

Capital Injection of 33% of cost of project

Business owners and aspiring entrepreneurs will be required to show their commitment to the proposed project by making an equity investment of their own money. Thirty-three percent of (33%) of the project costs must be injected by the owners or primary principals of the company. Generally, the equity contribution comes from the borrower’s savings, family, friends and associates.

Three Years Industry Experience

The borrower should be able to show that a key Principal involved in the business has relevant experience in the industry. As an example, ideally the owner of a new start-up restaurant will be able to show prior work experience in managing all aspects of a restaurant or a similar retail business.

Detailed Business Plan

To determine the viability of the loan request, the borrower is required to provide a detailed business plan showing how the proposed business will become viable with the ability to repay the loan request. The plan should be thorough covering all aspects of the business including, marketing, sales, operations, management, competition, industry statistics, demographics, pro-forma balance sheet, income and cash flow projections, underlying assumptions, etc.)’ The projections should be provided month to month over a two-year period and include underlying assumptions explaining how the numbers were derived.

Sound Credit History

Perhaps one of the most important factors in determining a company’s ability to repay a loan is the character of the owner. HBDI will review the credit reports of individual principals of the borrowing company as a component of determining character. Any Principal of the company with 20% or more ownership in the business will be required to allow an investigation of their personal credit history. While do consider individual credit scores, a low credit score will not always be viewed negatively. We will also look at the underlying factors behind the score and consider reasonable explanations. Ongoing late pays, unpaid collections, public records of liens, etc. are each derogatory items that may hinder the chances of favorable consideration.

Secondary Source of Income

Initially, the projected cash flow for a start-up company may not be sufficient to support the proposed loan. Accordingly, a secondary source of income outside of the business i.e., employment, a spouse’s wages, retirement or disability income, income from rental property, etc., will be considered favorably when considering the loan request.

Collateral

The proposed loan will be secured by any existing business assets that are unencumbered, as well as by the assets purchased with the loan proceeds. Collateral may consist of equipment, real estate, furniture and fixtures, vehicles, and accounts receivable. Because lenders typically will discount assets for depreciation and other factors required for liquidation, we typically will require ideally 1:1 coverage of assets to debt. Should the business assets alone prove to be insufficient to cover the proposed loan, personal assets may also be considered.